There are only eight Hurst Cyclic Principles that define the way in which financial markets are influenced by cycles. Each one of these principles is important in defining the Hurst Cycle approach to analyzing a market, but one of the principles always strikes me as more important than the others, and that is the Principle of Variation.

The Principle of Variation states that the cycles that influence financial markets have expected average wavelengths (and amplitude and other characteristics), and that actual instances of those cycles will tend to vary from the average. In simple terms this means that a 40-day cycle in the market will have a wavelength that is not exactly the average wavelength of that cycle.

The Principle of Variation is “more important” than the others I believe because it is not a simple black-and-white principle. It is sometimes mistakenly viewed as the “cop-out” principle because it used to mitigate analysis statements. It should not be dismissed because of this, but should instead be focussed upon so that we understand the implications of the principle correctly.

Hurst never answered the question: “how much variation is too much?”, but when developing Sentient Trader I had to answer that question because computers do like things to be black-and white (or 0 or 1)!

For instance we know that a 40-day cycle has an average wavelength of 34 days (we call it the 40-day cycle because that is easier than saying “the 34-day cycle” – OK, this is a bad example, but 5-day cycle is easier than saying 4.3-day cycle … well, let’s move on). And so we expect the actual wavelength of the cycle to vary from the average length of 34 days. But how much variation is acceptable and how much is too much? Clearly if a cycle is 60 days long it is more likely to be an instance of the longer 80-day cycle (which has an average wavelength of 68 days).

Sentient Trader resolves this issue by using a range of 65%-150% of the average wavelength as a suitable variation. When it comes to the 40-day cycle that means that a cycle which has a wavelength of 22 – 51 days is considered valid.

That is all very well, but what if you have a cycle that is 51 days long and another cycle that is 52 days long? Is the former a 40-day cycle, and the latter an 80-day cycle? There is only a one day difference between them, and so it is surely absurd to be so “black-and-white” about it! Yes indeed, and Sentient Trader isn’t so “black-and-white” about it, it uses a form of fuzzy logic to resolve these situations, which includes looking at the shorter cycles and how they have formed.

Why am I going on about this? Because the markets (which given the opportunity to entertain us with an analytical puzzle will always do so) are currently presenting us with exactly this situation: a 40-day cycle that is 51, 52 or 53 days long (depending on the market). There are several ways of resolving this situation in terms of one’s analysis, and in today’s ST Outlook I will present the various options that I think are most likely.

S&P 500

As discussed last week it seems likely that the first 40-day cycle since the 4 June 2012 40-week cycle trough occurred on 12 July 2012. However Wednesday’s trough occurred exactly 51 days after 4 June 2012 and so it is possible that is the correct position for the trough. If we position the 40-day cycle trough on 12 July 2012, as shown in the chart below, then there is a further puzzle to resolve: is the trough on Wednesday 25 July 2012 of 10-day or 20-day magnitude? At 13 days in length either option is possible.

I have been discussing for a few weeks the fact that I expect an early peak in the current 40-week cycle, and an email this week prompts me to mention just “how early” I expect the peak. Here is the longer term picture again:

The buy and sell turning zones show graphically what I mean by “an early peak”, but here is the logic:

- The current 40-week cycle should have a lower peak than the previous 40-week cycle (lower than 1420 in the S&P 500), and it should occur in the first 20-week sub-cycle. The reasons for this have been discussed previously.

- The first 20-week sub-cycle mentioned above is the current 20-week cycle of course, and so where do we expect the peak of this cycle to occur? The underlying trend of this cycle is neutral to slightly bearish and so the peak is expected in the first 80-day sub-cycle (or it could occur early in the second 80-day sub cycle).

- The underlying trend of the first 80-day cycle (which is playing out now) is bullish, and so we expect the peak of this 80-day cycle in the second 40-day sub-cycle.

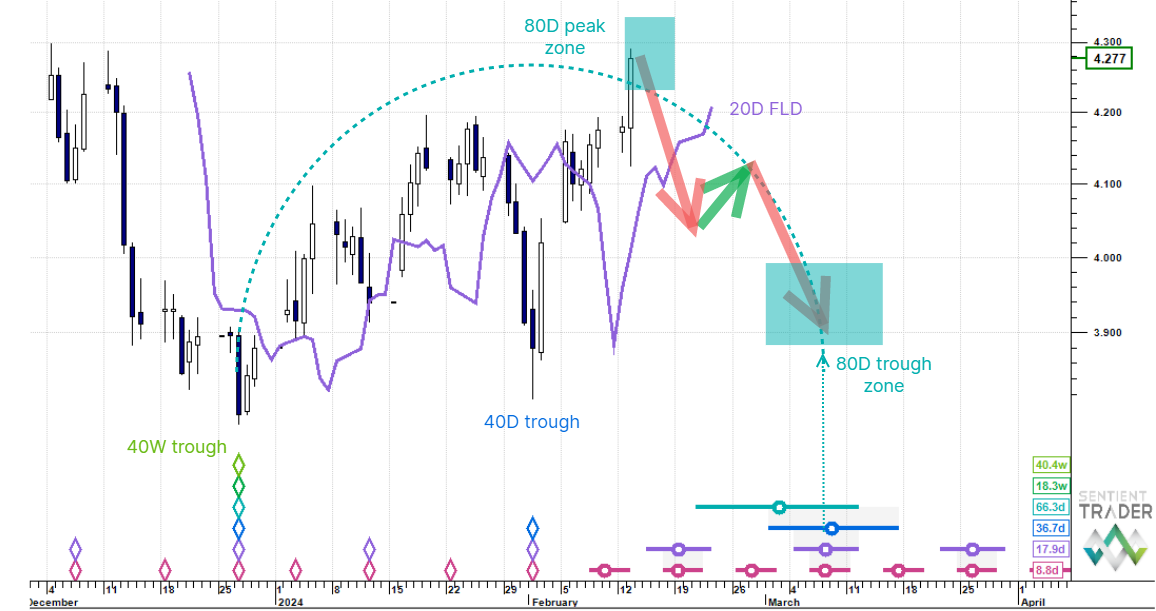

Nasdaq

The situation is the same in the Nasdaq, and so let’s take a look at something else of interest: the interplay between price and the 20-week FLD. I mention above that the peak of the current 40-week cycle in US markets is expected in the first 20-week cycle, and we will know that peak has occurred when price crosses below the 20-week FLD. Here is that FLD. Note how price travelled along the FLD in early July, and then bounced off the FLD this week on Wednesday.

Euro/US Dollar

The Euro presents the same puzzle with regard to the placement of the 40-day (and perhaps longer) cycle trough, but it pushes the envelope a bit further with a 53-day cycle instead of a 51-day cycle. The two analyses we have been tracking are still both viable, although the initial strength of the bounce this week make this analysis seem more likely:

That implies a very long 27 & 1/2 week cycle for the most recent 20-week cycle, which is not impossible (the principle of variation strikes again!)

The other option is this:

This option is more bearish as discussed previously, and implies that the trough on Tuesday this week (24 July 2012) is of 40-day magnitude. The bounce out of that trough looks stronger than the bounce out of a 40-day cycle trough, but I am treating the rise with some caution. There is a lot of “fundamental noise” present in the Euro at the moment, which could create exactly such a strong bounce. When I say “treat with caution” I do not mean that one should stay out of the market, but that stops should be placed carefully.

Gold

Gold finally showed what it was made of this week by breaking out of the triangle that we have been watching. In the process it broke the 20-week FLD, and tipped the scales in favor of one of the analyses we have been tracking, which implies that it will soon form the expected peak of the 40-week cycle, as shown here:

Of course the fact that it is going to form a 40-week peak soon is not very bullish, because it will turn down quickly from that peak. The alternate analysis that I have presented is still possible, and I will be watching the current rise carefully. If it continues with strength (on increasing volume) then the possibility that the 40-week peak has already occurred and is a straddled peak will become more likely. Cycles are often long in gold (as Hurst pointed out) which is why I favor the analysis shown above.

30 Year US Bonds

Bonds struggled up to a higher peak this week and left in place a 51-day cycle between the June peak and Wednesday’s peak. Here I present another way of resolving the variation issue, which is to identify one of the peaks (or troughs if considering a normal, non-inverted analysis) as a false peak, usually the result of fundamental interaction. In this case the analysis views the peak in early June as a “false” peak, and indeed it does look as if some fundamental interaction might have caused a surge upwards, which was corrected within days.

It is possible that when most markets were undergoing their 40-week cycle turns, the bond market suffered from some “fundamental tremors” as a result, although I usually prefer the simpler approach which is that the June peak was of 40-day magnitude, and we have seen a long 40-day cycle since then. But either way it would seem that bonds have now formed their 18-month cycle peak.

Crude Oil

Crude oil is the one market that does not present us with the long-cycle puzzle, because it formed the 40-week cycle trough later than the other markets, on 28 June 2012. It is forming a 40-day cycle trough now, which might have occurred on Wednesday this week, or there might be another dip lower to form the trough. Note how price is still above the 40-day FLD, implying that the Wednesday trough is premature for a 40-day cycle, but given that most other markets have turned with at least 40-day strength this week, and that the underlying trend on the 40-day cycle is so bullish, it is quite possible.

I have mentioned before that I am expecting the current 40-week cycle in oil to be of bearish shape, and I would like to clarify what that means. Here is a chart indicating the shape of the cycle that I expect in oil:

As you can see, although the cycle is bearish in shape (early, lower peak and lower closing trough) does not mean that oil prices will be falling constantly from now. The current bull move is expected, and is part of the cycle shape. Cycles are after all cyclical, and have up and down legs.

US Dollar Index

The US Dollar squeezed out another peak this week, but then fell sharply. We have been expecting a fall into the 20-week cycle trough, and it would seem that is now happening. As it turns out the Dollar doesn’t have much further to fall in order to form a valid 20-week cycle trough below the 20-week (and 80-day) FLD’s:

That’s it for this week! A final comment about the distinction between analyzing markets and trading them. I have discussed today the puzzle of where to place the 40-day cycle turning point, which is a fascinating analytical puzzle. If your interest is purely in trading you might well say “who cares whether the trough is here or there?” As long as you are making trading decisions using Hurst’s Cyclic tools, the exact position of the trough is often of purely academic interest, and your comment would be perfectly valid. It is an example of the “robustness” of Hurst’s Cyclic Principles: you don’t have to be 100% correct in order to be profitable.