Evidence has been mounting recently that the cycles which move the stock markets of the world have been “running short”. Two weeks ago John mentioned it in his post about the 4-Year Presidential Cycle. This week José suggested it as the reason behind this week’s strong bounce up in Hurst Chat (the social side of Hurst Signals), and I have been bothered for many months by the fact that troughs seem to be forming on the “syncopated beat”, indicating that they are either running short, or possibly long.

To receive these blogs as soon as they are posted Join/Like/Follow Us. If you don’t do social media – click to Join Feedburner to receive these blogs by email.

If indeed the cycles are running short then it is possible that the trough formed in the first week of February is in fact a trough of 18-month magnitude. I have been discussing an approaching 40-week trough here, but could that trough be a bigger one?

Here is a chart of the S&P 500 (ES futures contract) which shows that possibility:

This analysis shows the 18-month (and 4 & 1/2 year) cycle trough in November 2012. I have highlighted the big problem with that position for the trough – 409 days or 13 & 1/2 months is very short for an 18-month cycle. I will come back to that cycle length in a moment, but if we accept it as an 18-month cycle, then this is how things look at the moment:

Notice the nest-of-lows for the 18-month cycle trough, which is due now. (If you want to do this analysis in Sentient Trader you need to build a simple expert model with the 18-month cycle).

But let’s go back to that very short 409 day “18-month” cycle between October 2011 and November 2012. In June last year I wrote a post (The 50-day Puzzle) about how many clear cycle troughs were forming on the “syncopated beat”, exactly half way between their average length and the average length of the next longer cycle (or the average length of the next shorter cycle, depending how you look at it). In that post I discussed the formation of troughs at the 51 day and 101 day positions, and it is something that has continued to occur with increasing regularity. The average length of the 18-month cycle is 546 days, and the average length of the next shorter cycle (the 40-week cycle) is 273 days. Isn’t it interesting that the syncopated beat of those two cycles, the point exactly mid-way between the two wavelengths is 409 (& 1/2) days? And so the “very short” cycle from October 2011 to November 2012 is in fact simply another example (on a larger scale) of the 50-day puzzle I wrote about last year.

Sentient Trader incorporates the Principle of Variation into the analysis it performs, but when cycle troughs occur at exactly the mid-point between where you would expect cycle troughs to occur, the “handling” of that variation is tested to the extreme. I have been wondering whether this constant formation of troughs at the in-between points is perhaps an indication that all the cycles we monitor have lengthened or shortened, and so I created a nominal model which differs from Hurst’s, and specifies cycle lengths which are two-thirds of their usual length. Here is the result of an analysis using that nominal model:

Now perhaps I’m weird, but to my mind that is a beautiful analysis. Notice the near-perfect regularity of the cycles, and the very narrow future cycle trough positions, or nests-of-lows, which can be seen more clearly here:

Narrow nest-of-lows indicate that there is very little variation in the cycle wavelengths, and is often an indication of a good analysis.

And so I think there is a good deal of evidence that the cycles are currently running short (at about two-thirds of their usual wavelength). Should you throw out your Hurst nominal models, and adopt this shorter wavelength model? No, I don’t think so. Perhaps I’m old-fashioned but I think that this “quickening” of the cycles is a temporary thing and that we will see them expand again. I found that the nominal model defined by Hurst in the 1970’s still applied in the early 2000’s when analyzing up to a hundred years of data in many markets. The current distortion might last several years, but I expect the cycles to return to “normal” eventually.

Trading in the face of analysis uncertainty

An obvious question is: “how is it possible to make sensible (and profitable) trading decisions if the cycles we are trading might be running at only two-thirds of their usual length?”

A fundamental aspect of any trading strategy is that it should enable you to make profitable trading decisions even when there is some analysis uncertainty. The FLD trading strategy does this very well, and to demonstrate this here are two charts from Hurst Signals (which uses the FLD trading strategy):

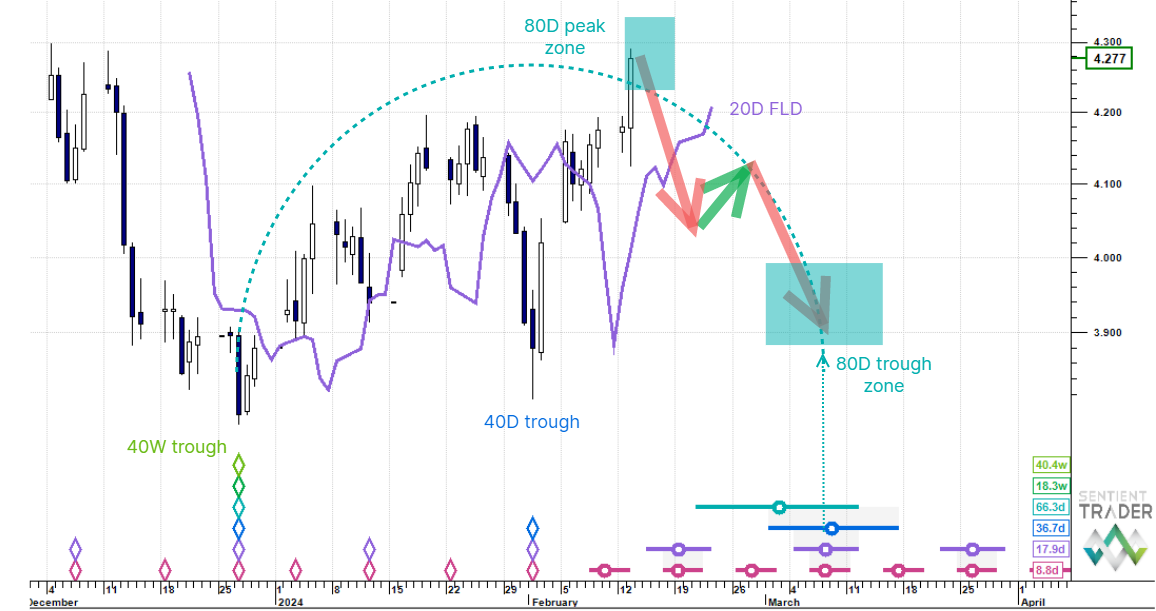

This analysis is the one we’ve been discussing here over the past few weeks, and it has the early February trough as a trough of the 40-day cycle (a 50 day long cycle!), which is still possible. The long E-category trade taken as price crossed the FLD (that purple line) has already been very profitable, even if that trough might actually be a trough of the 18-month cycle instead of the 40-day cycle.

Here is a different analysis in the Dow Jones Industrial Average:

Here the trough was expected to be of 20-week magnitude, and the A-category trade has also turned in a good profit.

And so which analysis is correct? Only time will tell of course, but fortunately we are still able to make profitable trading decisions while the analysts figure it out. With the strong move up this week I am tending towards the shorter cycle analysis at the moment. What do you think?

Have a good week and profitable trading.