For several weeks we have been preparing for the cycles to turn down in the US markets, which they did this week, forming a likely peak of the current 20-week cycle. The markets fought back on Friday, but trading volume was distinctly thinner, and the bounce smacked of a hopeful “the bull’s not done yet” sentiment, which is likely to fade as the fact that the cycles have turned is gradually accepted. Cycles might be suppressed and their troughs become hidden (as discussed last week), but eventually they all turn (with apologies to Shakespeare for the misquote).

S&P 500

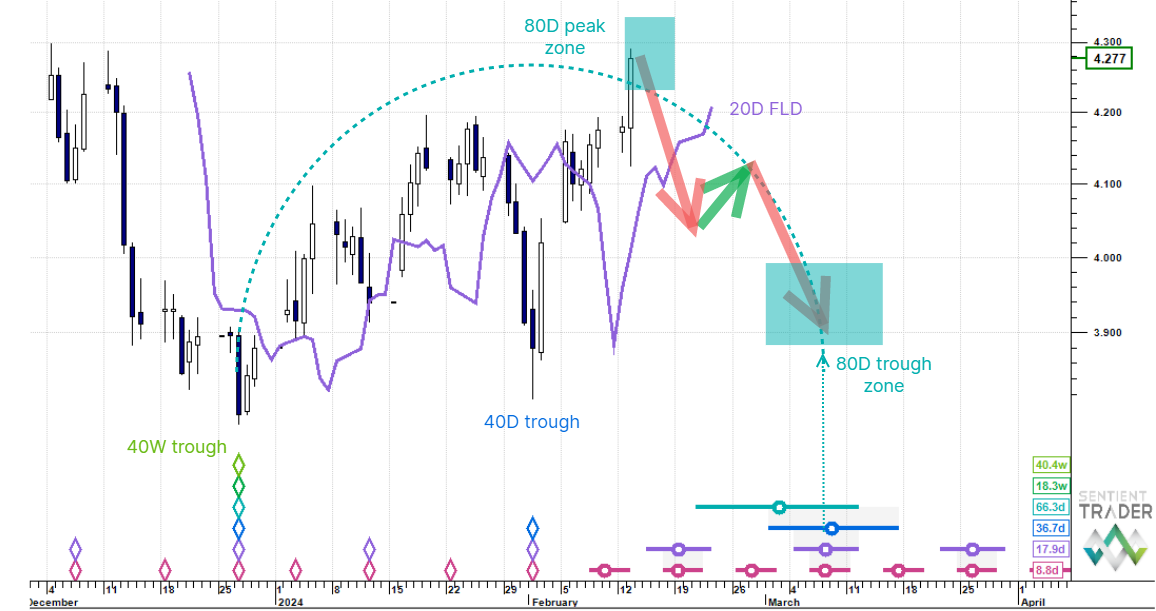

I mentioned last week that we could see a straddled 40-day cycle trough following the hidden 80-day cycle trough in early February. Thursday’s low was probably the 20-day cycle trough on the way to that 40-day cycle trough, indicating that the market will fall further into the 40-day cycle trough, then bounce up into the second peak of the current 80-day cycle. This second peak is likely to be fairly symmetrical with Wednesday’s peak, and might exceed it, but if the preferred analysis that we have been tracking holds true then it is likely to be a lower peak as the longer cycles bear down into the 18-month cycle trough.

I have been tracking the alternate analysis in the Nasdaq, but it is also of course a viable analysis for the S&P 500. Here is that analysis:

This analysis has the cycles running generally shorter, and so the nest of lows that the market is heading down towards is expected earlier (late March as opposed to April-May), and will be a trough of only 20-week magnitude, not 18-months. Under this analysis the second peak discussed above could quite possibly exceed Wednesday’s peak.

This is my less preferred analysis. More important at the moment is to be wary of the downside potential of the preferred analysis.

Nasdaq

Here is the analysis that we have been following in the Nasdaq:

This analysis positions the 80-day cycle at the end of 2012, giving us a short 80-day cycle following the mid-November trough, as would be expected if that November trough was a trough of the 18-month cycle. Recent price action has been compressed into a narrow range making the identification of cycle troughs a challenge, but here too the Thursday trough looks likely to be a trough of the 20-day cycle, and the market is expected to keep falling into the 20-week cycle trough expected in March.

Euro/US Dollar

The Euro continued falling this week, and it is not clear whether the 40-day cycle trough has formed (as a hidden or subtle trough), or whether it is still forming now. The 40-week cycle shape is clear however, and as mentioned previously the 40-day cycle trough is likely to be little more than a hesitation on the way down to the 40-week cycle trough expected in March.

Gold

Gold has been falling from the subtle 80-day cycle peak formed in January this year. The strong move down of the past two weeks does not change the analysis, but it does paint a more bearish cycle picture. I am still expecting a bounce up into the 20-week cycle peak in about May, but it is important to remember that peaks (and troughs) can have a magnitude that is not commensurate with the cycle that is forming them. As this cycle shape becomes more bearish we need to revisit the issue of the magnitude of the September 2011 peak. As discussed previously this peak might be of 18-month magnitude, or of 54-month magnitude. The more bearish the current cycle shape becomes the more likely it is that the September 2011 peak was of 54-month magnitude. The long-term implications of that would be bearish, as we would not expect prices to exceed that peak for several years.

30 Year US Bonds

I suggested last week that the 80-day cycle peak of early February might prove to be a straddled peak with symmetrical price action surrounding the peak, and as Bonds climbed a little higher this week that seems even more likely.

Crude Oil

Last week I explained why it was likely that the 40-day cycle trough which formed on 11 February 2013 would be a straddled trough, with symmetrical price action on each side of it, and as the price of Crude Oil fell this week that prediction proved to be a very profitable one. The cycles have clearly turned down for oil, and price is falling now into the 18-month (possibly 54-month) nest-of-lows centered around March this year.

US Dollar Index

For two weeks now I have been considering the magnitude of the 1 February 2013 trough in the US Dollar. As the dollar continued upwards this week it makes it more likely that the trough was the 18-month (perhaps 54-month) cycle trough that we have been expecting. It is still not impossible that the dollar will fall into a lower trough as shown in this analysis, but it is becoming less likely with each bullish day. If it turns out that the February trough was of greater magnitude than 40-days then the phasing of the troughs since the September 2012 trough is not perfect, but we cannot expect the markets to be perfect all the time!

That’s it for this week. If you are getting started with Hurst cycles then make sure you take advantage of our February getting started special which ends this week.

Have a great week and profitable trading!