I am often asked “In what markets do Hurst Cycles work best?”

I have always answered that Hurst Cycles work equally well in any liquid, well-traded market. But I now qualify that statement, by adding: ” … to the extent that it is not being manipulated”. The word manipulation generally has a negative implication, and so let me clarify that by manipulation I mean “any attempt to influence” … it is not necessarily a negative or evil manipulation!

To receive these blogs as soon as they are posted Join/Like/Follow Us. If you don’t do social media – click to Join Feedburner to receive these blogs by email.

I think this concept is a very important one to consider now as we are seeing more and more examples of (more and more complex) manipulation in the markets we trade.

When the European Central Bank announced its fairly extraordinary Quantitative Easing program this week, I started wondering what effect this would have on the markets, if any.

I do expect the ECB’s QE plan to have an effect on the markets, but I don’t expect it to have the effect of prolonging the bull market indefinitely. In fact I don’t expect it to have much of an effect on the direction of European stock markets generally. (For a good quick explanation of the intended effect of QE take a look at the video here).

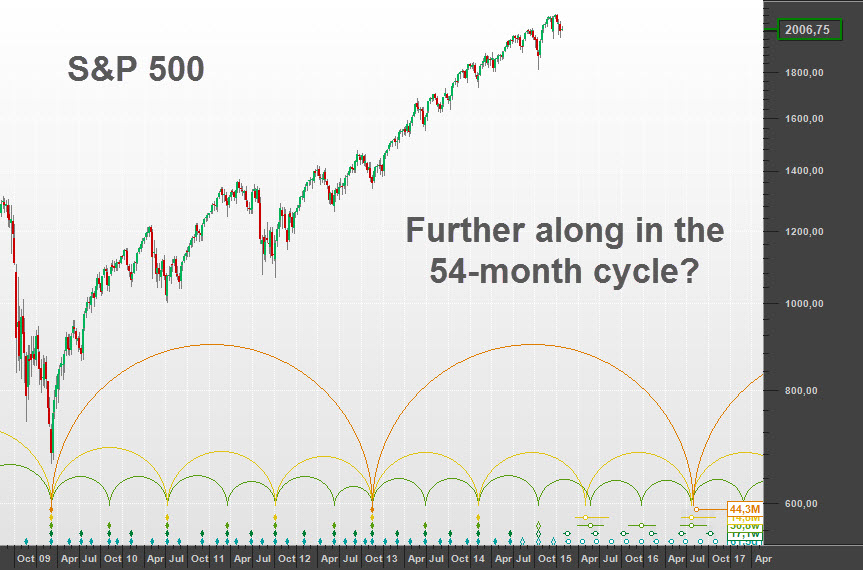

A divergence between the European and the US markets started developing recently, and I discussed this in my latest Hurst Trading Room podcast. I believe that the divergence is caused by the fact that the US markets are a bit further along in the current 54-month cycle than the European markets. Here is the S&P 500:

And the DAX:

Looking at those charts can we honestly say that we can see the effects of QE in the US? I think that perhaps we can, but not in the way that most people would expect. The big trough in March 2009 was not an effect of QE in my opinion, nor were any of the other peaks or troughs.

The effect that I think we can see is in a distortion of the cycles in the market. This distortion is often difficult to “see”, but it does have a dramatic effect on our analysis and trading of the cycles.

I am suggesting that any manipulation of a financial market (and QE is a manipulation in that it is an “attempt to influence”) does not succeed in changing the fundamental cycle structure of that market, but it does distort the market, making it more difficult to trade from a cycle perspective.

Any manipulation of a financial market does

NOT succeed in changing the fundamental cycle structure of that market,

but it DOES distort the market, making it more difficult to trade from a cycle perspective

In other words if financial markets were completely “free” and not subject to any form of manipulation then I think we would see very clear cycles, and trading those cycles would be a much simpler affair.

I also think that all markets experience varying degrees of manipulation at different times, and a corollary of my suggestion above is that the success of trading any financial market on the basis of a Hurst Cycles analysis is inversely proportional to the amount of manipulation that market is being subjected to.

If you are interested in reading about a practical demonstration of this idea then please read the full post here: http://hurstcycles.com/markets-and-manipulation/

In conclusion, although I do not expect the ECB’s QE plan to change the overall direction of the European stock markets (which are destined to form a major trough within the next three years), I do expect that the QE plan is going to make trading those markets from a Hurst Cycle perspective more difficult.